Lingerfelt targets office properties that offer long-term income durability, repositioning potential, and alignment with modern tenant expectations. Our strategy focuses on both acquisition and development opportunities that serve healthcare providers, professional services, and corporate users in growth-oriented markets.

Market Focus:

Target Sub-Types:

| Class A and select Class B Professional Office | Government or Institutional Tenancy Anchors |

| Distressed Value-Add Opportunities | Office to Medical Conversions |

Lingerfelt targets office assets with strong tenancy fundamentals and value-add potential through leasing, repositioning, or capital improvements. We focus on well-located properties serving healthcare, government, or professional users, and execute with speed, discretion, and certainty.

We partner with healthcare systems, corporations, and institutional users to deliver tailored office solutions. From site selection to delivery, our integrated approach ensures cost control, speed to market, and long-term functionality.

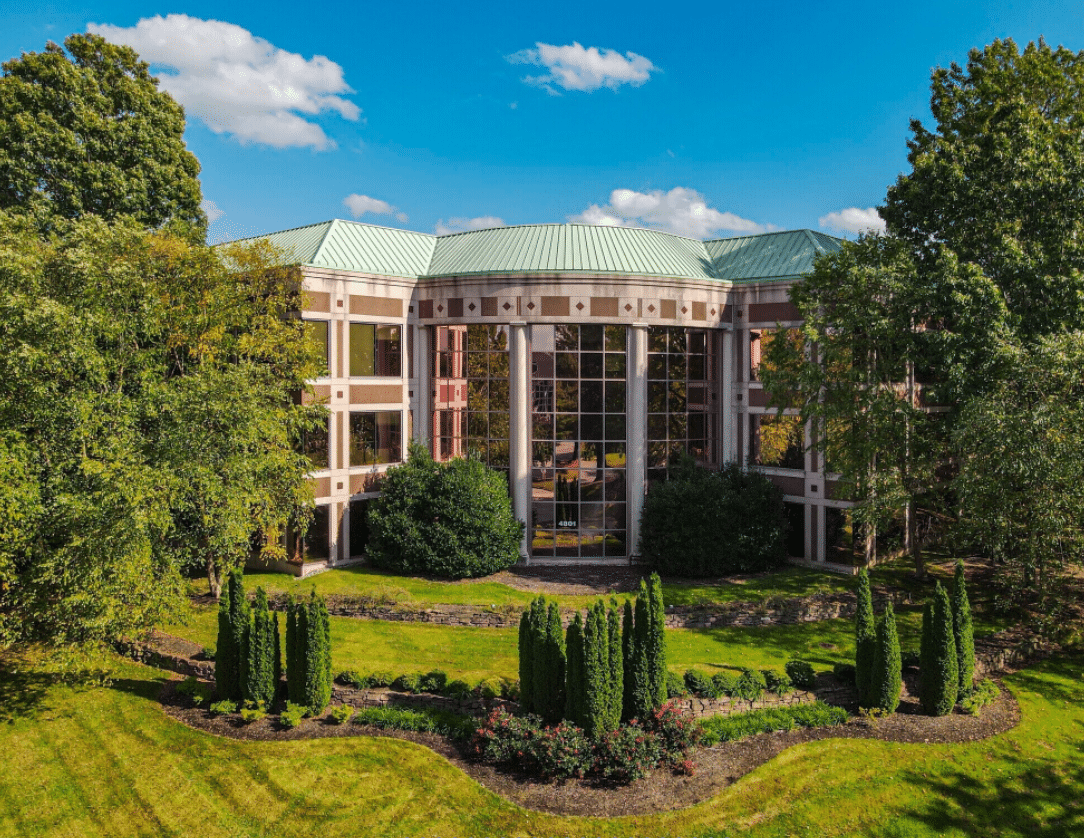

When acquired in 2013, the Innsbrook Office Portfolio consisted of 14 suburban office buildings totaling nearly 1 million square feet in Western Henrico County, Virginia. At the time, the portfolio was approximately 98% leased, featuring a diverse mix of over 90 tenants with an average occupancy of around 10,000 rentable square feet each. Many leases were locked in at below-market rates, offering long-term upside potential through strategic leasing and repositioning efforts.

The Innsbrook portfolio grew in 2014 with the strategic acquisition of additional office space from a regional real estate investment trust, further strengthening the our presence in the submarket. Over the course of the investment period, select assets from both the original and expanded portfolios were sold in phases as market conditions and loan provisions allowed. These included three buildings from the original acquisition and all buildings from the expansion portfolio. During the final year of the hold period, we successfully rezoned 5 of the 7 remaining parcels to Urban Mixed Use designation, allowing for the future construction of apartment buildings on the surface parking lots. This rezoning unlocked untapped future value in the land parcels, allowing us to market the portfolio as a redevelopment play. The final disposition included 11 office buildings totaling over 700,000 square feet, bringing the Innsbrook investment full circle and completing our effective exit from the submarket.

In mid-2022, the remaining 11 properties within the Innsbrook Office Portfolio were placed under contract and successfully sold later that year to Seminole Trail Management, concluding the final chapter of our long-term investment. The portfolio’s performance over the nearly decade-long hold period reflected strong value creation through disciplined asset management, strategic leasing, favorable market timing, and strategic rezoning efforts. The execution of the lion’s share of the Innsbrook assets during the Covid-19 pandemic represented a highly complex execution with returns well exceeding expectations given the circumstances.

The acquisition of Riverplace Tower occurred in an off-market transaction at a purchase price of $29M, or $66 per square-foot. The value-add business plan outlined prior to acquisition and executed during the hold period included parking structure upgrades, operating expense reduction via management changes, lease-up of vacancy via marketing team changes, and capitalizing on rising rental rates and compressing cap rates. Lingerfelt successfully maximized revenues and minimized costs through effective in-house property and asset management. A significant portion of the value creation that Riverplace Tower experienced was due to management’s ability to increase net rents by 40% throughout the hold period, in part by reducing operating expenses by 10% while at the same time increasing gross rental rates by 16%. As the original business plan forecasted, the Riverplace Tower investment benefited from improving market fundamentals within Jacksonville’s Southbank. The business plan was renewed under the same value-add strategy with the recapitalization of the investment in November of 2016, whereby a previous JV equity partner was replaced by a new investor group.

At acquisition, Southbank class-A office vacancy hovered around 10.4%, subsequently dropping to 6.6% as of Q3, 2016. Along with strong realized absorption, the Southbank also saw meaningful rent growth. Since late 2014, the Southbank saw asking rates increase over 16% as of Q3 2016. Due to these improving market fundamentals, during our hold period, the Jacksonville Southbank experienced meaningful cap rate compression, generating a highly favorable environment for disposition. Our decision to stay in the investment through recapitalization was rooting in our belief that there was further untapped value in additional lease-up and rent growth. This was realized during the second iteration of the investment with occupancy jumping from 85% to 91% and NOI increasing 41%.

Through the 7-year overall hold period for the Riverplace Tower investment (2 year initial hold period + 5 year post-recapitalization hold period) the asset experienced 180% NOI growth with occupancy rising from 70% to 91%. Market sale timing for both the recapitalization and the final exit were on target with cap rates of 6.5% and 5.6%, respectively. The ability to execute the recapitalization of the investment allowed original investors to crystallize returns while allowing new investors to participate in additional apparent value upside. Investors in both the original transaction and the recapitalization realized returns well above original underwriting expectations.

The acquisition of Hampton Roads occurred in an off-market transaction at a purchase price of $84 per square-foot. The value-add business plan outlined prior to acquisition was centered around rent, occupancy, and weighted average lease term growth across the portfolio. The portfolio was approximately 87% leased at the time of acquisition, with additional lease-up to be driven by capital improvements to bring the assets to Class A market standard.

During the hold period, average rents were increased 8.3% from $17.05 to $18.47, occupancy was grown 3% from 87% to 90%, and the portfolio weighted average lease term was increased from 2.92 to 3.08 years. Subsequently, NOI growth from acquisition to disposition totaled $2.7M, rising from $11M to $13.7M. The portfolio value increase can be largely attributed to this NOI growth. Additionally, tenant improvement costs were mitigated at $7/RSF on a weighted basis, versus our underwritten expectation of $13/RSF, greatly reducing required capital outlay and cost basis expansion. During the hold period, 340k RSF in new deals and 600k SF in renewal transactions were executed across 138 transactions. LCP also successfully maximized revenues and minimized costs through effective, vertically-integrated in-house property and asset management.

As the original business plan contemplated, the initially identified threats to the investment were effectively mitigated creating further upside in the above fundamental growth, NOI growth, and cap rate compression:

1.) Lack of Liquidity – we were able to take the portfolio to market and identify a strong buyer despite the size of the market and scale of the portfolio;

2.) Depth of Market – despite historically weak but rebounding market fundamentals going into the investment, the Hampton Roads market experienced healthy rent and occupancy growth during the hold period; and

3.) Defense Based Leases –despite a heavy exposure to defense-based tenants, increased national military spending allowed us to lock in new and existing defense-based tenants on longer lease terms without contract-based termination rights.

The resulting investment returns greatly surpassed underwritten expectations on a compressed timeline.